2 Newly Launched Loan Apps in 2025: Transforming Quick Financing in India

India’s fintech revolution is in full swing, and 2025 is bringing exciting new players to the digital lending space. With the growing demand for instant, hassle-free loans, newly launched loan apps are empowering Indians to meet their financial needs—be it for emergencies, business growth, or personal aspirations. These apps leverage cutting-edge technologies like artificial intelligence (AI) and UPI integration to deliver seamless, transparent, and inclusive lending solutions. In this article, we dive into two standout loan apps launched in 2025: Finanable and another innovative platform we’ll reveal later. Designed with Indian borrowers in mind, these apps are set to redefine how you access credit in today’s fast-paced world.

Why Loan Apps Are Booming in India in 2025

Digital lending is transforming India’s financial ecosystem, with the market expected to grow significantly in the coming years. According to industry estimates, India’s digital lending sector is projected to surpass ₹10 lakh crore by 2030, driven by increasing smartphone penetration, UPI adoption, and the need for quick financing. Loan apps eliminate the hurdles of traditional banking, such as lengthy paperwork, branch visits, and rigid eligibility criteria. With features like instant approvals, flexible repayment options, and AI-driven credit scoring, these platforms cater to diverse groups, including salaried professionals, small business owners, and those with limited credit history. In 2025, apps like Finanable and our yet-to-be-named second app are leading the charge with user-friendly interfaces and competitive offerings tailored for India.

Finanable: Your Go-To App for Instant Loans in India

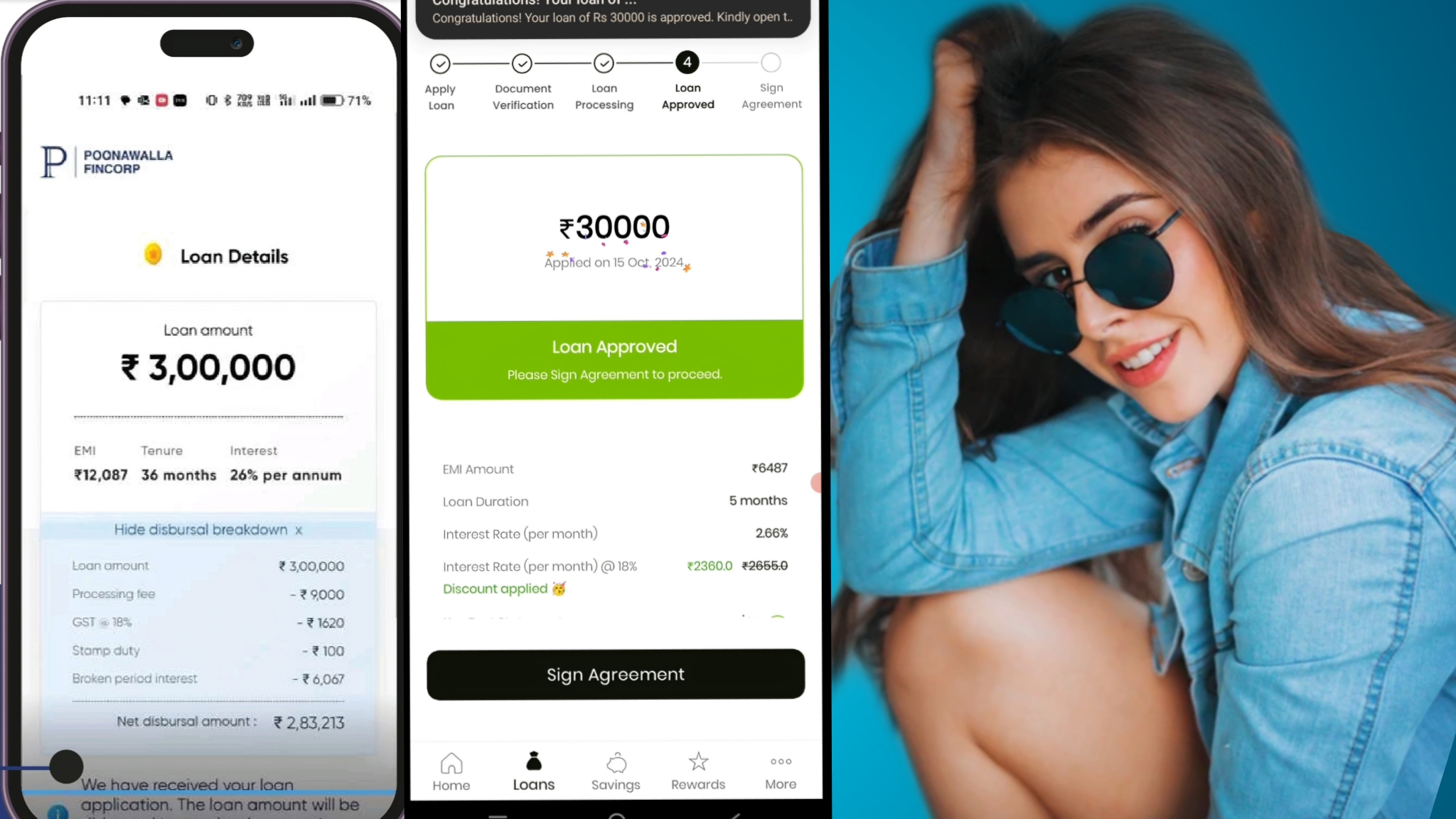

The first app on our list is Finanable, a trailblazer in India’s digital lending space. Launched in early 2025, Finanable is designed to provide fast, collateral-free loans to individuals and micro-businesses across urban and rural India. Whether you need funds for medical emergencies, wedding expenses, or to scale your small business, Finanable offers a seamless borrowing experience through its intuitive mobile app, available on Android and iOS.

Key Features of Finanable:

- Loan Range and Flexibility: Finanable offers loans from ₹5,000 to ₹5,00,000, with repayment tenures ranging from 3 to 36 months, making it suitable for varied financial needs.

- AI-Powered Credit Scoring: Using advanced AI, Finanable assesses creditworthiness by analyzing alternative data like UPI transaction history, utility bill payments, and behavioral patterns, ensuring accessibility for those with no formal credit history.

- Instant Approvals and Disbursals: Loan applications are processed in minutes, with funds credited to your bank account via UPI or direct transfer within hours.

- Transparent Pricing: Finanable ensures no hidden charges, with interest rates starting at 10% per annum, depending on the borrower’s profile.

- Localized Support: The app supports multiple Indian languages, including Hindi, Tamil, and Telugu, and offers 24/7 customer support via WhatsApp and call centers.

Finanable is a favorite among young professionals, gig workers, and small shop owners who value speed and simplicity. With over 1 lakh downloads within months of its launch, it’s gaining popularity in cities like Mumbai, Delhi, and Tier-2 towns alike. User reviews praise its quick processing and responsive support, positioning it as a top choice among newly launched loan apps in India for 2025.

The Second App: A Game-Changer for Indian Borrowers

Now, let’s unveil the second app, which is set to transform how Indians manage their finances. Say hello to Better Place Money, a 2025 launch that combines lending with financial empowerment tools. Unlike conventional loan apps, Better Place Money goes beyond offering credit by providing budgeting tools, credit score insights, and savings challenges, making it a holistic financial companion for Indian users.

What Makes Better Place Money Unique?

- Tailored Loan Offers: Better Place Money uses machine learning to customize loan amounts and interest rates based on your financial profile, ensuring affordability.

- Microloan Options: For small, urgent needs, the app offers microloans starting at ₹1,000, perfect for students or daily wage earners.

- Financial Wellness Tools: Features like expense trackers, credit score monitoring, and goal-based savings plans help users achieve long-term financial stability.

- UPI Integration: Seamless loan disbursals and repayments via UPI make transactions quick and convenient.

- Ethical Lending: The app promotes inclusive financing, with special loan schemes for women entrepreneurs and rural borrowers.

Better Place Money resonates with millennials, Gen Z, and small business owners who seek flexibility and transparency. Its focus on financial literacy and ethical lending makes it a standout, with early users lauding its intuitive design and value-added features.

Why These Apps Stand Out in India’s Competitive Market

Finanable and Better Place Money are tailored for India’s diverse borrower base, addressing pain points like delayed approvals and complex processes. By leveraging AI and UPI, they offer instant, inclusive financing that aligns with India’s digital-first economy. Their competitive interest rates, multilingual interfaces, and focus on underserved segments like rural borrowers and women entrepreneurs give them an edge. Additionally, both apps comply with RBI regulations, ensuring trust and security for users.

To rank high in search results, these apps optimize their online presence with keywords like “instant loan apps India 2025” and “new personal loan apps.” Their app store descriptions and websites target long-tail keywords like “quick loans without CIBIL” and “best loan apps for small businesses in India,” capturing users searching for specific solutions.

Tips for Choosing the Right Loan App in India

With numerous loan apps available, picking the right one can be daunting. Here’s how to make an informed choice:

- Compare Interest Rates: Look for competitive rates. Finanable’s 10% starting rate and Better Place Money’s tailored offers are great options.

- Check Reviews: Platforms like Google Play Store reveal user experiences. Finanable has a 4.4 rating, while Better Place Money scores 4.6.

- Evaluate Features: Prioritize apps with tools like microloans, UPI integration, or financial planning features based on your needs.

- Ensure Security: Verify RBI compliance and data encryption for safe transactions.

- Test Support: Opt for apps with responsive customer service, preferably in regional languages.

Conclusion: Embrace India’s Digital Lending Revolution

The launch of Finanable and Better Place Money in 2025 marks a new chapter in India’s fintech journey. These apps blend innovation, accessibility, and user-centric design to make financing inclusive and convenient. Whether you prefer Finanable’s lightning-fast approvals or Better Place Money’s holistic approach, both are excellent choices for navigating India’s financial landscape. Download them today from the Google Play Store or App Store and take control of your financial future!