New Loan App Fast Approval-₹15000 loan

In today’s fast-paced world, managing finances efficiently is crucial. Whether it’s handling unexpected expenses, paying utility bills, or indulging in online shopping, having instant access to credit can make life stress-free. Enter New Loan App, India’s credit super-app designed to offer instant loans, Buy Now Pay Later (BNPL) options, utility bill payments, vehicle management, and gift card purchases—all in one user-friendly platform. With a focus on transparency, security, and convenience, this app is transforming how over 20 lakh Indians manage their financial needs daily. This SEO-optimized article explores the features, benefits, and unique offerings of New Loan App, making it your go-to solution for seamless financial management.

What is New Loan App?

New Loan App is a versatile, all-in-one financial platform that combines the convenience of instant personal loans, BNPL services, utility bill payments, vehicle management tools, and gift card purchases. It’s designed to simplify your financial life by offering a free credit limit of up to ₹10,000, which you can use across 45,000+ online stores and merchants. The best part? You repay the total amount every 15 or 30 days, completely interest-free, with no hidden charges. With its paperless, 100% digital process, New Loan App ensures a hassle-free experience for salaried professionals, self-employed individuals, and students alike.

Key Features of New Loan App

New Loan App stands out with its diverse range of features tailored to meet various financial needs. Here’s a closer look at what makes it India’s preferred credit super-app:

1. PayLater: Shop Now, Pay Later with Ease

The PayLater feature allows you to shop effortlessly across thousands of merchants with a single tap. Whether you’re ordering food from Swiggy or Zomato, shopping for fashion on Myntra, or grabbing essentials from Zepto, New Loan App lets you use your credit limit without the hassle of OTPs, CVVs, or PINs. Key highlights include:

- One-Tap Payments: Checkout seamlessly with no delays.

- Interest-Free Credit: Shop and repay every 15 days without extra costs.

- No Hidden Fees: Enjoy complete transparency in transactions.

- Exclusive Discounts: Avail attractive offers on popular platforms like Swiggy, Zomato, Myntra, and more.

By completing a quick and simple KYC process, you can unlock a higher credit limit of up to ₹5 lakh and extend your repayment period to 30 days, giving you double the flexibility. If you’re unable to clear your dues in one go, New Loan App offers EMI options for added convenience.

2. BillPay: Simplify Utility Bill Payments

Managing utility bills has never been easier. With New Loan App, you can pay electricity, gas, water, mobile prepaid/postpaid, landline, DTH, and FASTag recharges using your credit limit. The app supports over 20,000 billers, ensuring all your payments are covered in one place. Key benefits include:

- One-Click Payments: Pay bills instantly with minimal effort.

- Flexible Repayment: Clear your dues every 15 or 30 days alongside your New Loan App bill.

- Wide Coverage: From utility bills to FASTag recharges, manage all payments seamlessly.

This feature eliminates the stress of juggling multiple payment platforms, making New Loan App a one-stop solution for your billing needs.

3. Auto360: Your Vehicle Management Hub

For vehicle owners, New Loan App introduces Auto360, an all-in-one vehicle management tool. This feature helps you stay on top of your vehicle-related responsibilities, ensuring a smooth and stress-free ownership experience. With Auto360, you can:

- Track Challans: Stay updated on traffic fines and avoid penalties.

- Monitor Expiries: Get timely reminders for PUC and insurance renewals.

- Renew Insurance: Seamlessly renew your vehicle insurance within the app.

Auto360 simplifies vehicle management, saving you from last-minute surprises and keeping your ride road-ready.

4. GiftCards: Shop Smart, Save Big

Looking to gift something special or score discounts on your purchases? New Loan App offers gift cards for over 200 brands, including Amazon, Myntra, Flipkart, and more. These vouchers come with discounts of up to 30%, making them perfect for personal use or gifting loved ones. Whether it’s shopping for fashion, electronics, or groceries, New Loan App ensures you save while you spend.

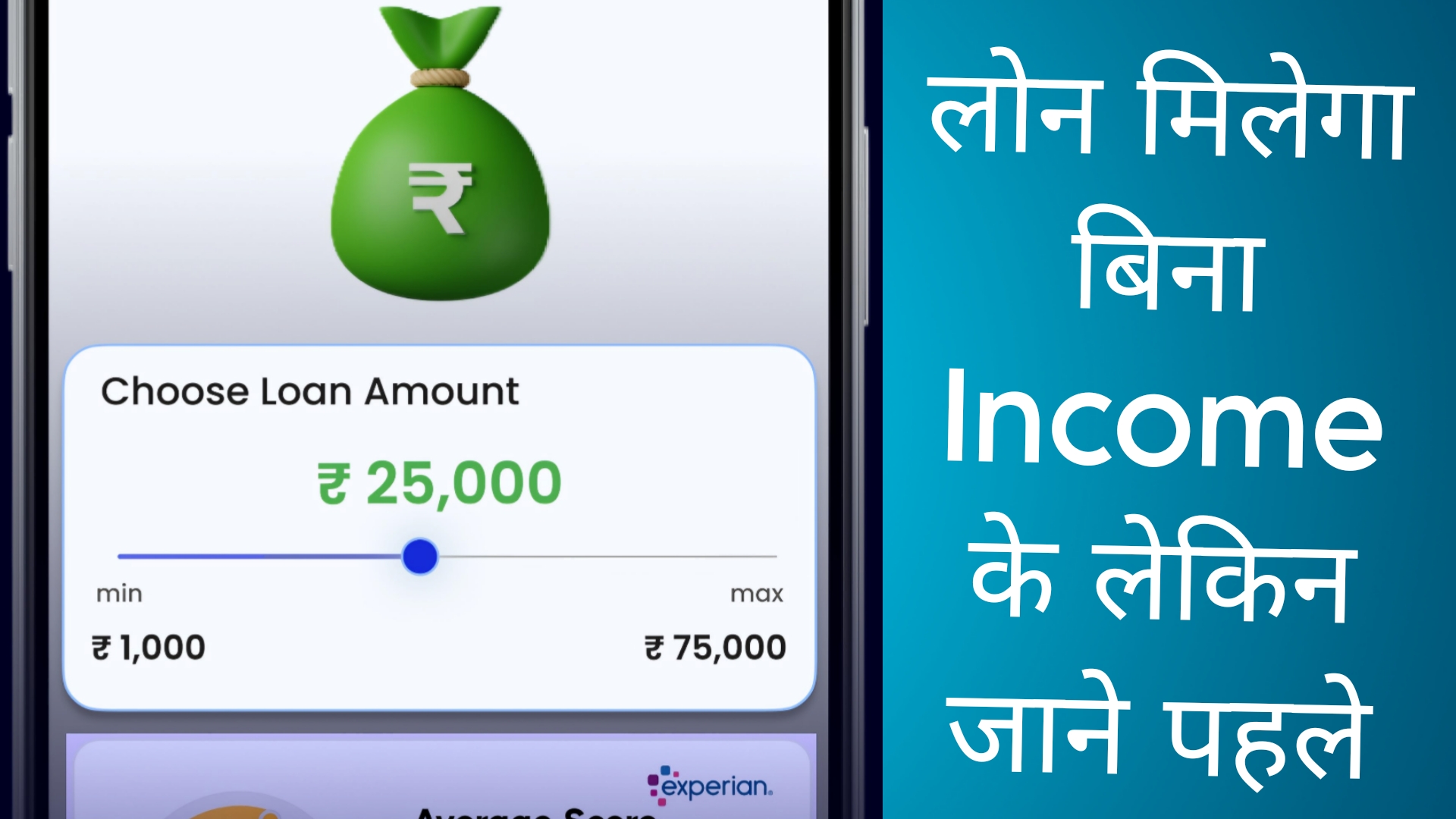

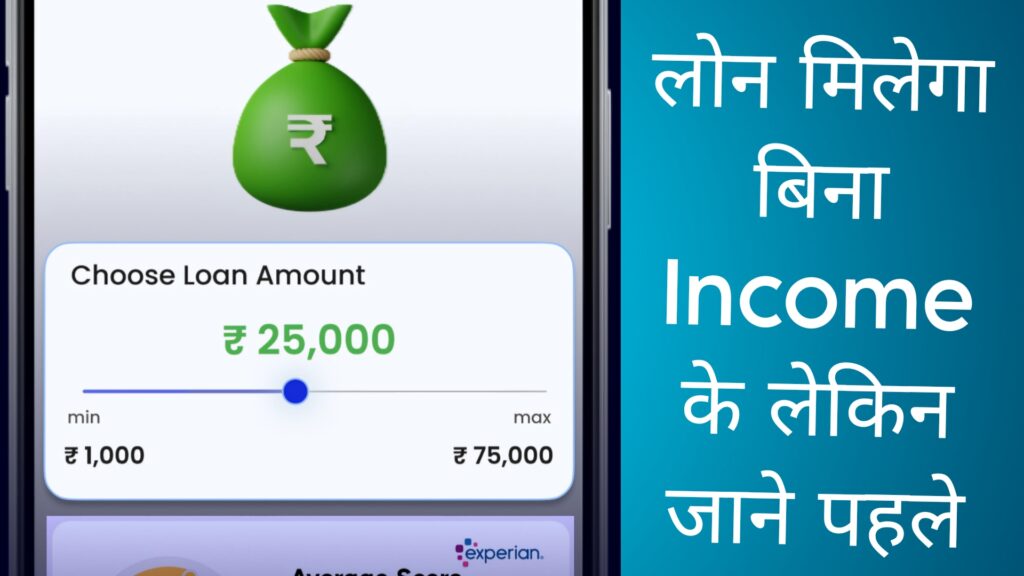

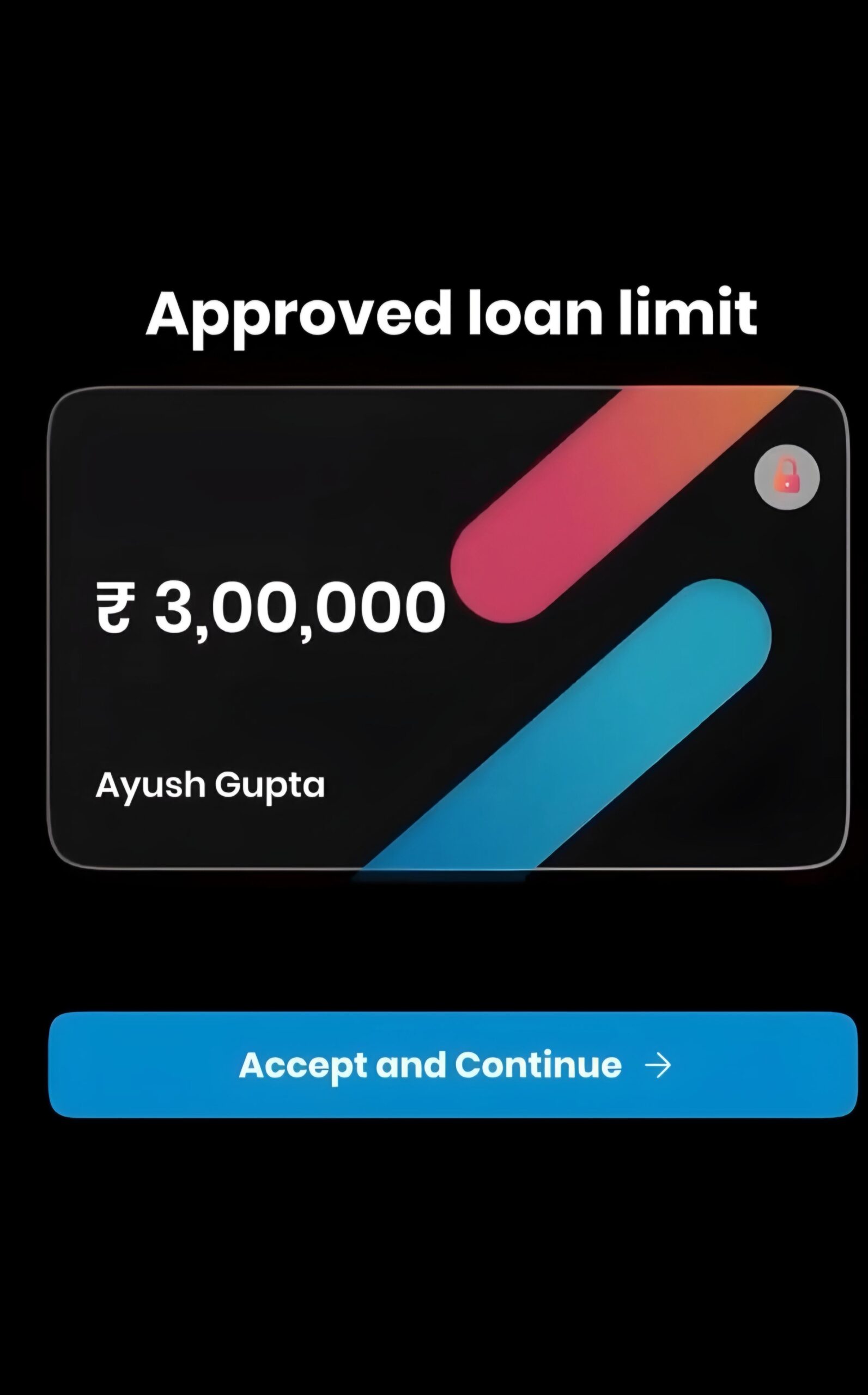

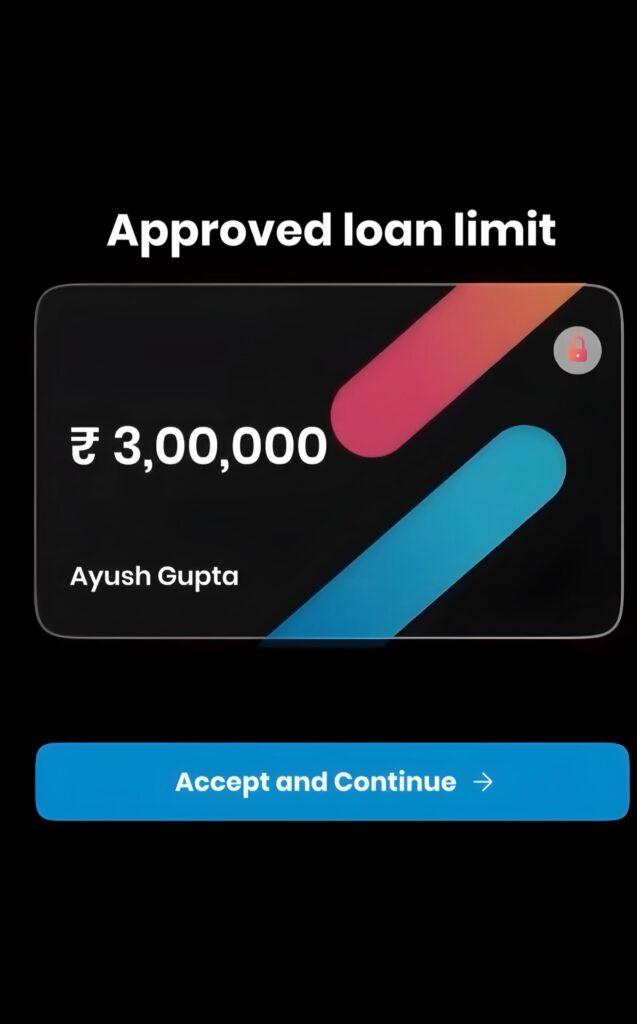

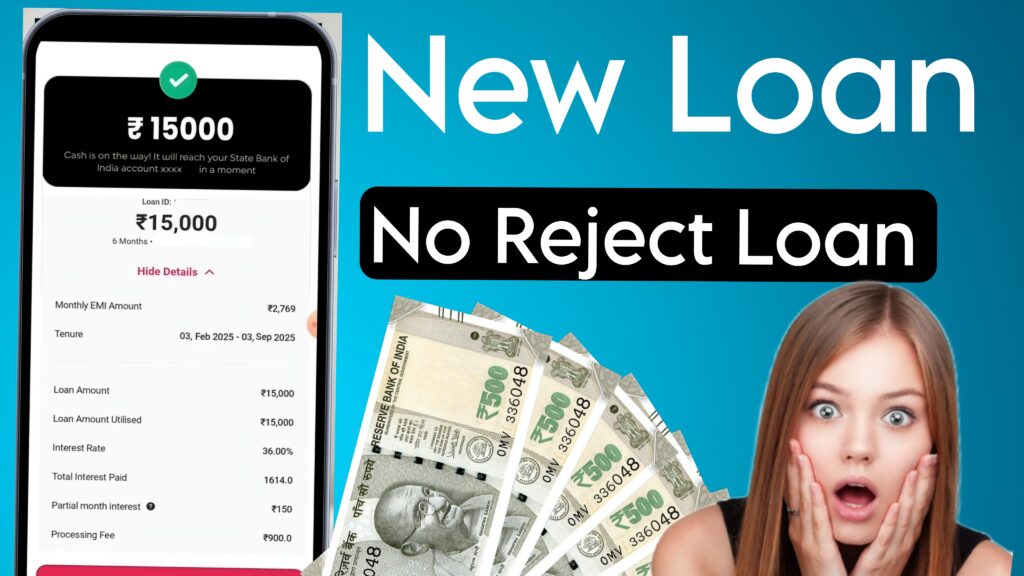

5. XpressLoan: Instant Personal Loans for All Needs

For those unexpected expenses or planned purchases, New Loan App offers XpressLoan, providing instant personal loans ranging from ₹3,000 to ₹5 lakh. The process is 100% digital, paperless, and requires no collateral, making it accessible to everyone. Key features include:

- Quick Disbursal: Get funds transferred to your bank account within minutes.

- Flexible Tenure: Choose repayment periods from 3 to 60 months.

- Competitive Rates: Interest rates range from 12% to 36% per annum, calculated on a reducing balance basis.

- Sample EMI Calculation: For a ₹10,000 loan with a 6-month tenure at 18% p.a., the EMI is ₹1,755 per month, with a processing fee of ₹200, totaling ₹10,730.

Additionally, the Revolve feature offers a monthly rolling credit line with rates between 36% and 42%, which can be converted to EMIs (3 months at 24% or 6 months at 26%) for added flexibility.

Why Choose New Loan App?

New Loan App is more than just a loan app—it’s a comprehensive financial tool designed to empower users. Here’s why it stands out:

- Transparency and Security: The app prioritizes data safety, adhering to RBI’s Fair Practices Code and partnering with registered NBFCs like PayU Finance India Private Limited. All your information is secure, giving you peace of mind.

- User-Friendly Interface: The app’s intuitive design ensures easy navigation, even for first-time users.

- No Credit Score Barriers: Even if you have a low or no credit score, New Loan App offers credit-building opportunities, making it inclusive for students and young professionals.

- 24/7 Support: Have questions? Reach out to the support team at wecare@lazypay.in for prompt assistance.

- Wide Reach: With over 20 lakh users and partnerships with 45,000+ merchants, New Loan App is trusted across India.

How to Get Started with New Loan App

Getting started with New Loan App is simple and takes just a few minutes:

- Download the App: Available on Google Play Store and App Store.

- Complete KYC: Submit your PAN and Aadhaar details for quick verification.

- Access Credit Limit: Unlock a free credit limit of up to ₹10,000, expandable to ₹5 lakh upon KYC completion.

- Start Using: Shop, pay bills, manage your vehicle, or apply for an instant loan—all from one app.

Who Can Benefit from New Loan App?

New Loan App caters to a wide audience, including:

- Salaried Professionals: Cover urgent expenses or enjoy flexible shopping with PayLater.

- Self-Employed Individuals: Access instant loans without the need for extensive documentation.

- Students: Build credit scores and manage small expenses with low or no credit requirements.

- Vehicle Owners: Simplify vehicle management with Auto360.

- Online Shoppers: Enjoy discounts and interest-free credit at thousands of merchants.

Tips for Using New Loan App Responsibly

To make the most of New Loan App, consider these tips:

- Timely Repayments: Pay your dues on time to avoid penalties and maintain a healthy credit score.

- Compare Loan Terms: Review interest rates and EMI options to choose a plan that suits your budget.

- Leverage Discounts: Use gift cards and merchant offers to maximize savings.

- Stay Informed: Regularly check Auto360 for vehicle-related updates to avoid fines or lapses.

Conclusion

New Loan App is redefining financial convenience in India with its all-in-one platform for instant loans, BNPL, utility bill payments, vehicle management, and gift card purchases. Its user-friendly interface, transparent processes, and commitment to data security make it a trusted choice for over 20 lakh users. Whether you’re looking to shop interest-free, pay bills effortlessly, manage your vehicle, or secure an instant loan, New Loan App has you covered. Download the app today, complete your KYC, and unlock a world of financial possibilities with ease and confidence.

For any queries, reach out to wecare@lazypay.in and join millions of Indians who trust New Loan App for their financial needs.